Andy Burnham’s expected arrival in Downing Street may end Labour’s leadership crisis, but Dennis Shen says it has opened a far larger debate about Britain’s economic future. As markets assess the implications of a Burnham premiership, questions are emerging over fiscal policy, Britain’s vulnerability to bond market pressures and whether Labour may gradually move closer towards Europe by the next general elections

Less than two years after Labour’s election victory, Britain finds itself preparing for its seventh prime minister in a decade. Keir Starmer’s resignation has ended months of speculation and cleared a path for Andy Burnham to become Labour leader and prime minister within weeks.

Yet Starmer’s departure has not eliminated the deeper pressures confronting Labour. Britain still faces a proverbial three-way squeeze: fragile public finances, sensitivity in gilt markets and a strategic argument over Europe that may redefine the political landscape by the next elections.

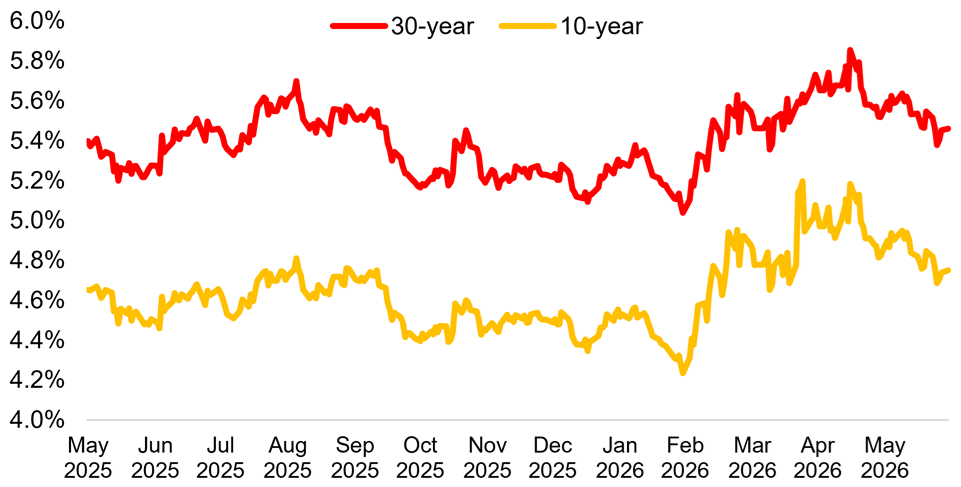

For much of 2026, political uncertainty itself was the story. Gilt markets have rallied as the prospect of a prolonged Labour civil war has faded. But one question has simply replaced another: what type of government will Burnham lead?

The recent global bond market rout – intensified by the Iran war – exposed the structural vulnerabilities of the British economy. UK gilts have repeatedly proven more fragile than many comparable sovereign debt markets during recent phases of global turbulence. The incoming government will prove as susceptible as its predecessors to such shifts in investor confidence.

The defining question of a Burnham premiership will be how far he seeks to shift Labour’s economic model.

Burnham is not a Corbynite. Yet he has long advocated a more interventionist state than either Starmer or Chancellor of the Exchequer Rachel Reeves, criticised Britain for being 'in hock to the bond markets' and argued for a more significant public role in economic development. Markets are therefore looking closely for two early signals: the contents of a planned economic speech and if he appoints a market-friendly Chancellor. Recent reports suggest Burnham targets greater flexibility within Labour’s fiscal framework while avoiding abandonment of the party’s fiscal rules.

That distinction matters.

Burnham’s allies argue there is scope for added borrowing to fund infrastructure, housing, and productivity-enhancing investment without undermining credibility. Investors may prove more receptive to such arguments if accompanied by a credible medium-term framework for debt sustainability.

Andy Burnham’s allies argue there is scope for added borrowing to fund infrastructure, housing, and productivity-enhancing investment without undermining credibility

The danger is that markets may hear flexibility and conclude that budgetary discipline is weakening. The lesson from recent British politics is that bond investors increasingly demand reassurances before granting governments room for manoeuvre.

A successful Burnham premiership may therefore hinge less on whether he spends more and more on whether markets believe that spending is linked to a coherent growth strategy.

Meanwhile, the mini-budget crisis of autumn 2022 remains in the public conscience.

Burnham may not be suggesting anything remotely comparable to the unfunded tax cuts pursued by Liz Truss and Kwasi Kwarteng. Nor has his emergence triggered panic in gilt markets.

Markets have welcomed the end of political uncertainty following Keir Starmer’s resignation. Yet that goodwill remains conditional

Indeed, markets have welcomed the end of political uncertainty following Starmer’s resignation. Yet that goodwill remains conditional. If Burnham’s economic programme is perceived as fiscally expansive without sufficient safeguards, gilt yields could begin rising again.

Much may depend on whether his Chancellor can convince investors that Labour remains committed to long-run debt sustainability.

One further source of relief remains external. Any durable peace agreement ending the Iran conflict would further ease inflationary pressures and support international bond markets.

The deeper issue is that Britain’s fiscal vulnerabilities are no longer cyclical. They are structural.

Successive governments have sought to square an increasingly impossible circle: maintaining elevated public spending, avoiding politically toxic tax rises, supporting ageing demographics, financing defence, and stimulating growth while reassuring bond markets that debt remains sustainable.

Burnham inherits exactly the same dilemma.

Labour’s fiscal rules sit awkwardly beside its ambitions to expand investment, repair public services, and accelerate growth.

The party argues that stronger growth can ultimately resolve such tensions. If productivity and investment improve, the fiscal arithmetic becomes less punishing.

Nevertheless, Britain has spent much of the past 15 years waiting for growth to solve its fiscal constraints. Markets may ultimately demand harder choices instead.

The campaign to replace Starmer has furthermore reopened a question of Britain’s relationship with Europe.

Last year, Burnham intimated his hopes of Britain rejoining the European Union within his lifetime. Yet during the Makerfield by-election campaign he was careful to clarify that rejoining is not an immediate policy objective.

That position is politically understandable. Nearer alignment with Europe could reassure investors and appeal to younger urban voters who still view Brexit as an economic drag. Yet Labour simultaneously faces pressure from Reform UK in constituencies where any overt move towards EU membership remains politically toxic.

Nearer alignment with Europe could appeal to younger urban voters, yet Labour also faces pressure from Reform UK in constituencies where any move towards EU membership remains politically toxic

The most likely outcome is therefore gradualism: closer cooperation with European institutions, deeper economic alignment, and a softer public conversation about Britain’s long-term place in Europe, without any near-term commitment around rejoining the EU.

A parallel question is electoral timing. Should Labour enjoy any meaningful polling bounce after Burnham enters Downing Street, pressure may grow for an early election to secure a personal mandate. Such a move cannot be ruled out entirely, but would carry substantial risks.

Britain’s current transition reflects something greater than any one prime minister.

The post-Thatcher settlement has weakened. Brexit has not produced a stable alternative growth model. Public expectations for state intervention continue to rise even as financial markets impose increasingly strict constraints on budgetary expansion.

The challenge confronting Burnham is therefore not simply to reunite Labour. It is to demonstrate that a more interventionist economic programme can coexist with market credibility.

That may become the defining test not only of Burnham’s premiership, but of Britain’s political economy in the years ahead.